After two years of hesitation, the art market suddenly found its appetite in New York.

After two years of hesitation, the art market suddenly found its appetite in New York.

July 9, 2026

The first half of the year has gone by. In the heat of the summer, the 2026 art market delivered the kind of auction headlines the art world had been missing. During New York’s spring marquee season, Christie’s, Sotheby’s and Phillips generated approximately $2.5 billion in sales, more than twice the comparable figure reported for the previous year. Christie’s led with roughly $1.45 billion, while Sotheby’s and Phillips contributed around $908.6 million and $146 million respectively.

Jackson Pollock entered the nine-figure club. Constantin Brâncuși crossed $100 million. Mark Rothko established a new auction record, and Joan Miró followed with one of his own. In one extraordinary evening, Christie’s sold more than $1.1 billion of art through the S.I. Newhouse collection and its 20th Century Evening Sale.

It would be tempting to declare the 2026 art market healthy again. The more accurate conclusion is narrower. The spring results showed that enormous capital remains available for works perceived as unique, institutionally validated and protected from the reputational risks surrounding recently traded material. They did not prove that demand has recovered evenly across artists, periods or price levels.

The 2026 revival was primarily a supply event. Three collections supplied the market with exactly what cautious buyers had been waiting for: S.I. Newhouse’s museum-grade modern masterpieces, Agnes Gund’s deeply personal holdings and Robert Mnuchin’s tightly edited group of postwar art. These were works that had been owned rather than merely warehoused, studied rather than rapidly flipped and kept away from auction long enough to recover the seductive aura of discovery.

The 2026 art market did not suddenly become less risk-averse. It found objects that made risk feel luxurious.

The season’s defining work was Jackson Pollock’s Number 7A, 1948, sold by Christie’s for $181.185 million. The price nearly tripled Pollock’s previous auction record and placed the painting among the most expensive artworks ever sold publicly. More importantly, it revealed how perfectly the 2026 market rewarded the combination of artistic importance, scale, rarity and long-term private ownership.

, oil and enamel on canvas, 35 x 131 ½ in. (88.9 x 334 cm.), painted in 1948")

Painted during Pollock’s breakthrough drip period, the canvas stretches more than three metres across. Its horizontal field records poured, flicked and tangled movements without resolving into a conventional image. The work had remained outside public view since 1977 before emerging from the Newhouse collection, transforming its return into an event rather than another auction appearance.

That absence mattered financially. A masterpiece repeatedly offered, exhibited at commercial fairs or passed between speculative owners can accumulate market fatigue. Number 7A arrived with the opposite condition: cultural familiarity attached to physical inaccessibility. Collectors knew Pollock’s significance, but very few had encountered this particular painting in person.

The sale also demonstrated that collectors will compete aggressively when an auction house can make substitution appear impossible. Buyers were not simply choosing between Pollocks. They were being asked when another monumental 1948 drip painting, supported by this provenance and preserved at this level, might return to market. The answer could plausibly be never.

Its seven-minute contest reportedly involved six bidders before reaching a $157 million hammer price. That visibility made Number 7A the season’s most convincing image of renewed confidence: real competition, an emphatic record and a work capable of carrying the result aesthetically.

Yet Pollock’s triumph should not be treated as evidence that Abstract Expressionism in general has entered a new boom. It proves that collectors will pay exceptional prices for an exceptional Pollock. In 2026, the distance between a masterpiece and merely good material may have widened rather than narrowed.

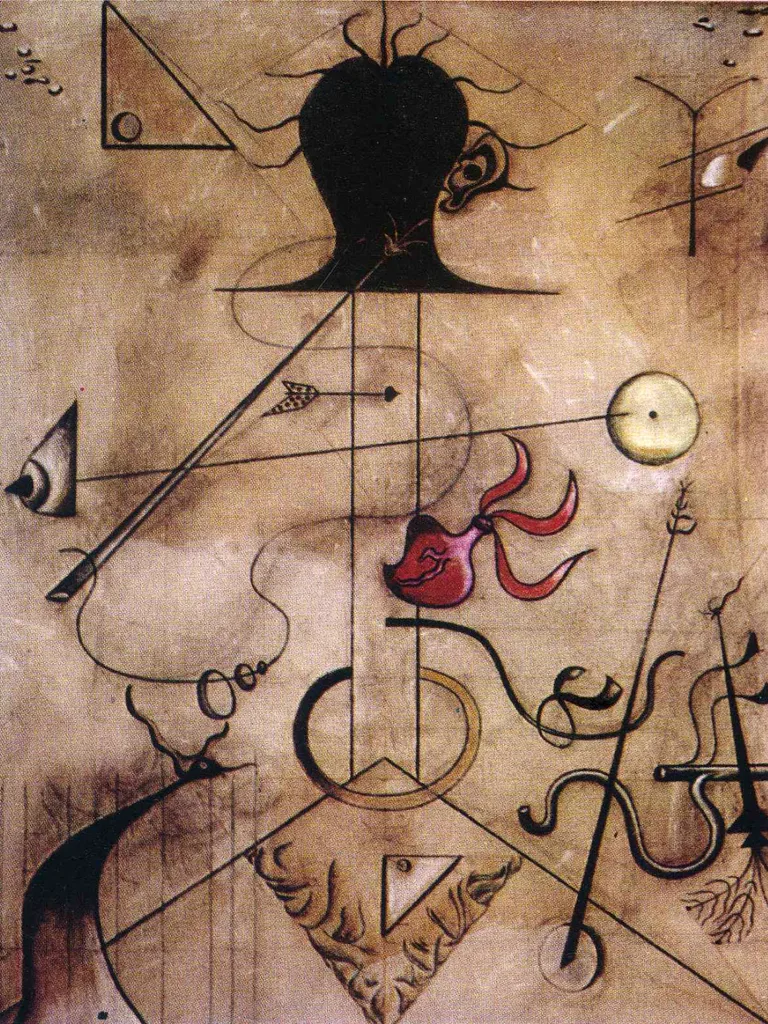

Constantin Brâncuși’s Danaïde, conceived and cast around 1913, realized $107.585 million at Christie’s, establishing a new record for the sculptor. The gilded bronze head reduces the features of Margit Pogány to an oval face, concentrated eyes and a dark, sharply articulated arrangement of hair. Its gold-leaf surface converts a small bust into an object that appears simultaneously ancient, mechanical and sacred.

, Danaïde, conceived and cast circa 1913. Bronze with gold leaf and black patina. Height (excluding base): 10⅞ in (27.1 cm)")

Its provenance was almost as distilled as its form. Historic collectors Eugene and Agnes Meyer once owned the sculpture before Newhouse acquired it in 2002 for $18.2 million, itself a record at the time. In 2026, Danaïde crossed the $100 million threshold and became one of the most expensive sculptures ever sold at auction.

The result strengthened the position of sculpture within the trophy market. Three-dimensional works have historically faced practical disadvantages: they require space, may exist in multiple casts and often lack the wall power of a monumental painting. Brâncuși overcomes those objections because his sculptures combine extreme formal recognition with tightly controlled production and an almost mythic place in the development of modernism.

However, the sale also exposes the carefully engineered nature of contemporary auction confidence. Danaïde was supported by a third-party guarantee and reportedly attracted only the guarantor at the decisive price level. Its $107.6 million result was historic, but it did not represent the same form of open competition as the Pollock bidding war.

The distinction matters. A guarantee secures a buyer before the auction and protects the seller from the humiliation of an unsold masterpiece. It can also give the 2026 art market reassurance that another financially sophisticated party has already accepted the work’s valuation. Yet the published price may describe a successfully managed transaction rather than spontaneous demand erupting in the room.

Mark Rothko’s two major results illustrated both the power of provenance and the precision of current taste. From Agnes Gund’s collection, No. 15 (Two Greens and Red Stripe) was sold at Christie’s for $98.385 million, setting a new artist record. Gund had acquired the 1964 painting directly from Rothko in 1967, giving it the purest possible ownership history after the artist himself.

At Sotheby’s, Brown and Blacks in Reds from Robert Mnuchin’s collection reached $85.78 million. Mnuchin had bought it in 2003 for $6.7 million, producing a dramatic increase that reflected both Rothko’s ascent and the premium attached to an important dealer-collector’s judgment.

Collectors were purchasing paintings, but they were also purchasing the intelligence of the people who had selected them.

The term provenance once sounded administrative: a chain of names required to establish ownership, authenticity and legal title. In the 2026 art market, provenance became a form of luxury branding.

Newhouse, Gund and Mnuchin did not merely possess expensive art. Each represented a recognizable collecting philosophy. Newhouse assembled works with graphic force and canonical importance. Gund combined museum leadership with philanthropy and sustained relationships with artists. Mnuchin brought the authority of a dealer who understood both connoisseurship and market structure.

Their names reduced uncertainty. A buyer approaching a recently made work may have to judge whether its primary-market success was constructed through scarcity, waiting lists and coordinated placement. An estate masterpiece arrives with decades of historical distance. Its value has already survived changes in taste, financial crises, museum scholarship and shifts in collecting fashion.

Joan Miró’s Portrait de Madame K. demonstrated how provenance can activate a work’s cultural history. The 1924 painting, once owned by Max Ernst, sold from the Newhouse collection for $53.535 million, establishing a new auction record for Miró. Its ownership connected it directly to the relationships surrounding early Surrealism rather than simply attaching a wealthy name to its catalogue entry.

This is the central lesson of 2026: buyers wanted objects with biographies. Long-term stewardship made a painting feel less like circulating inventory and more like a rediscovered cultural asset.

The preference also reveals anxiety. A market confident in its own expansion would distribute excitement across fresh names, new movements and recently produced art. A market recovering from contraction tends to retreat toward consensus. Pollock, Rothko, Brâncuși, Matisse, Picasso, Miró and Basquiat offer reputational infrastructure that younger artists cannot yet provide.

Provenance therefore functioned as both romance and insurance.

The 2026 rebound was not left entirely to chance. Sotheby’s $433.1 million evening of Mnuchin and contemporary sales was reportedly more than 80 percent guaranteed by value. Major works including the Pollock, Brâncuși and leading Matisse were also supported by third-party guarantees.

Guarantees are neither inherently deceptive nor unusual. They persuade owners to consign important works by promising a minimum return, while transferring some of the auction house’s financial exposure to outside backers. When bidding rises beyond the guaranteed level, the guarantor may receive a financing fee or share in the upside.

The structure creates liquidity, but it complicates the emotional theatre of auction. A sold lot does not necessarily mean that several new collectors independently endorsed its price that evening. In some cases, the eventual owner had committed before the catalogue was printed.

This helps explain why the high end could produce nearly perfect sell-through rates while parts of the wider market remained cautious. The trophy segment was insulated from failure through financial architecture unavailable to ordinary consignors.

Even the Newhouse sale, which achieved $630.8 million and sold every offered lot, contained signs of selectivity. Seven of its 16 works reportedly hammered below their low estimates. The collection’s total was immense, yet individual performance was uneven beneath the headline.

The guarantees do not invalidate the recovery. They define it. Confidence returned through a system designed to prevent public collapse.

The strongest 2026 results extended beyond the three largest records. Matisse’s La Chaise lorraine brought $48.405 million at Sotheby’s, nearly doubling its low estimate. Basquiat’s Museum Security (Broadway Meltdown) reached $52.718 million, becoming one of the contemporary season’s principal lots. Picasso, Miró and major postwar names added depth to a week dominated by 20th-century authority.

, oil on canvas, 129.5 by 89.2 cm, executed circa 1919")

Sculpture also gained visibility, from Brâncuși’s record to continued demand for museum-quality works by established modern sculptors. Still, a handful of exceptional results cannot yet prove that sculpture has achieved complete financial parity with painting. The supply of major sculptures is thinner, comparison is complicated by editions and casts, and the buyer base remains highly selective.

The first half of 2026 should therefore be read as a return of belief at the top rather than a universal art-market recovery. The season proved that sellers can still unlock extraordinary capital when they offer works combining rarity, canonical artists, respected provenance and carefully calibrated estimates. It also proved that auction houses have become highly skilled at manufacturing stability through guarantees.

What remains uncertain is whether the confidence will travel downward. The true test will come when the market faces good works without famous owners, expensive works without guarantees and contemporary artists whose reputations remain vulnerable to changing taste.

For now, the 2026 art market has rediscovered its nerve by looking backward. Its most powerful objects arrived from rooms assembled over decades, carrying the names of collectors who had already done the difficult work of choosing.

The $2.5 billion spring was spectacular, but its message was conservative. The 2026 art market plays it safe, as it offers something from the past that the market believed it would never see again.